Update to our Analysis and Valuation of Republic Protocol

This is an update to the full report by Blocktown Capital published in June 2018 on the analysis and valuation of Republic Protocol.

This is an update to the full report by Blocktown Capital published in June 2018 on the analysis and valuation of REN.

· Trustless privacy is a feature of privacy-centric blockchains, but is not available on Bitcoin, Ethereum and other programmable blockchains

· The RenVM brings decentralized, trustless privacy to Bitcoin, Ethereum and other blockchains

· While adoption of RenEx as a decentralized dark pool may take time, transaction and wallet privacy will likely be adopted on a much shorter time horizon

· Given the incentivization structure of the RenVM, namely fee generation, we use a discounted cash flow analysis to determine the present value of REN to be 2.47 USD

Disclaimer: The managing partners of Blocktown Capital own REN.

REN outperforms in depressed altcoin market

While the broader altcoin market cap is up 99% in 2019, REN is up nearly 400% for the year. REN is presently one of the best performing digital assets in 2019.

The price increase has not gone unnoticed and our team has received multiple requests for an updated analysis and valuation of Ren.

It has been a little greater than a year since we published the most comprehensive analysis and valuation of Ren to date. We believed then and continue to believe today that Ren has strong fundamentals that will result in value capture for REN.

Total Addressable Market of Ren is different in 2019

An updated discounted cash flow (DCF) analysis is warranted because key fundamentals of Ren have evolved. Our original DCF was based on projections of the trading volumes on RenEx, a decentralized dark pool for trading digital assets. However, over the past year, the Ren team is in the final stretch of accomplishing an — in our eyes — superior technical feat, which is bringing privacy and interoperability to Ethereum and most other large cap blockchains. This will be possible with the launch of Ren’s Virtual Machine (“RenVM”), to be released on testnet soon. The RenVM leverages zk-SNARK and secure multiparty computations to validate proofs and run programs in zero-knowledge. More details on the technical aspects of the RenVM can be found in their Litepaper.

We anticipate that the driving value of REN will be from the fees paid to Darknodes in return for trustless transaction privacy in the RenVM as opposed to the fees derived from trading on RenEx.

A trustless solution for privacy across blockchains has been sought after for years and continues to be a relevant subject today.

Vitalik Buterin also addressed privacy solutions for Ethereum multiple times over the past couple of months and even in this past week.

Privacy solutions currently consist of centralized tumbler services (e.g. BitcoinLaundry, CryptoMixer), wallets with built-in CoinJoin mixers (e.g. Wasabi) or select privacy-centric blockchains (e.g. Monero, Zcash). Layer 2 privacy solutions and dapps on Ethereum are actively being explored, but are still early in development and not yet on mainnet (e.g. Heiswap).

Ren not only brings privacy to cryptocurrency, but also allows interoperability across blockchains in the RenVM. That is, transactions on Ethereum, Bitcoin, Litecoin, EOS, Zcash, etc. — can be made private in the RenVM.

If the RenVM is successfully deployed, it will be the first scalable solution to bring privacy to not only Ethereum and ERC-20 tokens, but also to Bitcoin, Litecoin and many other large cap blockchains.

New assumptions for calculating a DCF analysis of REN

The value of REN is derived from trading fees and bonds. Fees are paid by users to Darknodes in exchange for privacy in the transfer of BTC, ETH, ERC-20 tokens (including USDT), LTC, EOS and other large cap digital assets. Bonds are submitted in REN by Darknodes in order to participate in the network. Each Darknode is required to hold a bond of 100,000 REN in order to receive fees from processing transactions. With this information and some basic market assumptions, we can model a DCF analysis to diagram the potential value of REN.

Assumption #1: Annual transaction volumes of Bitcoin, Ethereum, ERC-20 tokens (including USDT), Litecoin and other RenVM compatible coins will continue to increase.

Ethereum

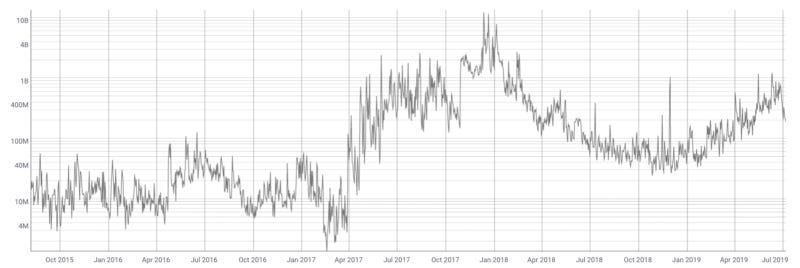

Since 2015, the daily USD value of ETH transactions continues to increase, as shown in the log scale graph below.

Averaging about 700M USD daily (250B USD annually) in 2019, we project the USD value of Ethereum transactions will continue to increase over the next few years to the values shown in Table 1.

Tether (USDT)

Averaging about 400M USD daily (150B USD annually) in 2019, we project the USD value of USDT transactions will continue to increase over the next few years to the values shown in Table 1.

ERC-20 Tokens

In 2019, the cumulative USD denominated amount of ERC-20 tokens (USDT excluded) transactions is estimated to be 150M USD daily (50B USD annually) with the vast majority from ERC-20 stablecoins (e.g. USDC, DAI, PAX). We project this number will continue to increase as the stablecoin market and decentralized finance (DeFi) economies grow.

Bitcoin

Averaging about 4B USD daily (1,500B USD annually) in 2019, we project the USD value of BTC transactions will continue to increase over the next few years to the values shown in Table 1.

Litecoin

Averaging about 300M USD daily (100B USD annually) in 2019, we project the USD value of LTC transactions will continue to increase over the next few years to the values shown in Table 1.

Table 1. Summary of Projected Transaction Volumes (USD billions)

Assumption #2: Fees for transactions processed by the RenVM will average 1 bps (0.01%).

The Ren team has specified that there are two types of processing fees in the RenVM — an “Upfront Fee” and “Incentivization Fee”. The upfront fee will be tailored to reflect the real-world cost of the proposed computation performed by the Darknodes. The optional incentivization fee will be further incentive for Darknodes to prioritize certain transactions.

It is difficult to project the exact fee amount as the RenVM has yet to be launched and the fees can be dynamically adjusted by the Darknodes. We do suspect that these fees will be more than the cost of typical mining fees but less than the cost of trading fees on the most affordable exchanges.

In 2019, Bitcoin transaction fees are hovering around 0.6 bps (0.006%) for the average transaction (average fee is ~1.50 USD and average transaction value is ~25k USD). Trading fees on exchanges commonly range between 5 bps and 20 bps (0.05% and 0.20%, respectively). The most affordable exchanges charge about 10 bps (0.1%) per trade. We anticipate that transaction and wallet privacy will be a coveted feature worth more than a typical mining fee of 0.6 bps but less than a trading fee of 10 bps. Let’s assume the upfront plus incentivization fees paid to Darknodes in the RenVM will be 1 bps of the transaction value.

Assumption #3: There will be 5,000 Darknodes participating in the RenVM.

This is 50% of the maximum 10,000 Darknodes allowed by the bond requirements (100,000 REN) and maximum supply of tokens (1,000,000,000 REN). Although there are many factors that will dictate the number of Darknodes active on the network at any given time, we feel comfortable modeling our assumption on other projects with similar node requirements.

Assumption #4: Transactions processed by the RenVM could approach 7.5% of total transaction volume over the next 3 years.

Transaction and wallet privacy can be accomplished in either base layer (core protocol) or layer 2 solutions. Currently, privacy on Bitcoin consists of centralized tumbler services which require users to trust often anonymous operators. This is not practical for large balances of cryptocurrency given the risk of theft. There is early progress on smart contract-powered, trustless solutions, such as Heiswap, but most are still largely unaudited and not yet on mainnet. Although there has been early discussion about incorporation of zk-SNARKs in future releases of the Ethereum protocol, progress has been slow. We anticipate that base layer privacy on Ethereum is still at least several years away, assuming layer 2 solutions for privacy don’t reduce the necessity and urgency for base layer privacy.

As the first mover in a scalable solution to bring privacy to Ethereum transactions, we suspect the RenVM will dominate transaction privacy. We project that up to 7.5% of all transactions could be made private through the RenVM by the year 2022.

Table 2. Projected Darknode rewards based on assumptions

Discounted Cash Flow Analysis

With these assumptions, we can calculate the price of REN based on the network fees paid to Darknodes, the largest holders of REN tokens.

Given Ren’s network incentivization, namely fee generation, we have decided again that the best valuation method would be a DCF analysis. Fees, which are to be paid in ETH, BTC, LTC or other ERC-20 tokens, can be substituted for a cash dollar amount in a typical DCF model. Similarly, one can envision a fee generating node as a dividend paying stock or an annuity paying bond that lasts into perpetuity (less the costs associated with the electricity and hardware used to run nodes).

Using the formula for DCF, PV = [CF1 / (1+r)1] + [CF2 / (1+r)2] + … + [CFn / (1+r)n] + TV, we can discount our cash flows back to present day to arrive at a Present Value (PV) for the REN network.

PV = Present cash flow value

CF1 = Cash flow at the end of year 1

CF2 = Cash flow at the end of year 2

CFn = Cash flow at n specified year

r = Discount or required rate of return

TV = Terminal Value

Before continuing further, we must assign a specific discount rate, r. Presently, there is no appropriate risk rate in the digital asset marketplace that can be used as a benchmark. As such, we will borrow from other financial markets to ascertain an acceptable discount rate. The risk free rate is typically deemed to be the return rate on US treasury bonds — a return which is considered to be devoid of risk of loss. Moving along the risk spectrum to a more appropriate discount rate, we arrive at funding costs for start-up companies. In Series A equity funding rounds for venture capital, the generally accepted rate is between 30–50% per annum. As a digital asset platform with certain technological components that remain unproven, Ren has a relatively high risk profile and we believe that it is reasonable to assign a discount rate that is similar to that of a Series A round for a startup. Given this information, we have decided to settle on a discount rate of 40%.

Using our estimates of fees paid to REN nodes from Table 2 above, we can plug these CF values into our formula.

PV = 0/(1.40)¹ + 18,000,000/(1.40)² + 108,000,000/(1.40)³ + 404,000,000/(1.40)⁴ + TV = 153,433,465 + TV

Lastly, we need to include those fees paid after the four year period. We model the REN platform to last into perpetuity, as is appropriate in the equity markets. To do this, we use the Gordon Growth Method to find a Terminal Value, TV. We conservatively model out a sustained growth rate of 2% (g = 0.02), in-line with mature company estimates.

TV = [year 4 cash flow * (1+g)/(r-g)]

TV = 404,000,000*(1.02)/(0.4–0.02) = 1,083,340,658

Adding up our yearly cash flows and terminal value, we arrive at the below summation:

PV= 153,433,465 + 1,083,340,658 = 1,236,774,123 USD

Finally, by dividing our total network cash value (1,236,774,123) by the number of anticipated circulating tokens (500,000,000), we arrive at a price per REN of 2.47 USD. That is, with our best assumptions, REN could achieve a value of 2.47 USD per token. This represents an upside of ~26x (2,600% ROI) from its current price of 0.09 USD.

One final note is that this analysis does not take into account any additional fees paid to Darknodes from RenEx and other decentralized dark pools on the Ren network. We have intentionally excluded this as we project that there will be significant overlap between fees paid for processing trades and fees paid for private transactions as all trades processed on the network will already be private. Nevertheless, one could argue that by excluding the fees collected from dark pools, we have arrived at a conservative present value for REN.

Summary

Assuming a successful launch of the RenVM, and the continued growth of the cryptocurrency economy, a DCF model projects the value of each REN token to be worth 2.47 USD — approximately a 2,600% ROI from its current price in July 2019.

This value is projected based on the anticipated value capture of providing a decentralized, trustless privacy and interoperability solution to Ethereum, Bitcoin, Litecoin, ERC-20 tokens and many other large cap blockchains. In a few short years, we may nostalgically remember the days before private transactions where alerts of Tether printing and whales moving large quantities of tokens to exchange wallets were commonplace.

Disclaimer

The managing partners do not endorse, or recommend any investment action in REN. This document should not be regarded as investment advice, offering document, or as a recommendation regarding a course of action. The managing partners of Blocktown Capital own REN. These views are those solely of the managing partners of Blocktown Capital and do not represent the views of the Ren team.